Blog

Whoever Said That Money Can’t Buy Happiness Simply Didn’t Know Where to Go Shopping

9/15/2020

PASPA, as previously understood, had effectively banned states from regulating or profiting from sports betting, leaving only a grandfathered few states with the ability or interest to offer sports betting the past few decades. Change came swiftly on the heals of the new interpretation that sports betting was and is not prohibited by PASPA- only a month later wagers were being accepted in Delaware and New Jersey. As you can imagine, many companies and investors saw this as the opening act for a tidal wave of opportunity.

I am convinced this was based on two things: 1) the enormity of the wager volume that has long been assumed to live in the shadows in the US, that oft-referenced $150bn figure, and 2) the appreciation that America is uniquely suited to be a large market for sports betting. Why? Unlike our neighboring betting markets in Europe, Americans have a much broader variety of sports and a broader distribution of engagement across sports. While the UK features many dedicated fans of specific teams, general football fans in the US follow many teams, many games, and many other sports. The US is already more obsessed with statistical analysis; Europe doesn’t call a bunch of video reviews on plays. Plus, the games themselves tend to be higher scoring, with more opportunity for betting.

Like many investors, we at Jump Capital were excited about the opportunity, so we spent some time looking into it in 2018. Not only was the category superficially interesting for the merits above, but it was also a logical fit for our focus in digital media. While the first order affect may be to benefit the gaming entities who are already active in the space, the rise of legal sports betting in the US instantly raises the value of media companies and sports content rights holders. It creates an entire new category of monetization for any traditional cable or OTT platform that can engage consumers and activate them as bettors, and it can fundamentally change the way that millions of fans across the US engage with sports, a category currently stemming the tide of cord-cutting and keeping many broadcasters in business.

Jump Capital’s HQ is in Chicago; here in Illinois our new governor, JB Pritzker, has been making a strong push to legalize sports betting. Many states are in a similar boat, but this close-to-home initiative has motivated us to publish some of our thoughts on the space.

The summary of that work is that yes, the US may well be fertile ground for sports betting, and in a rosy scenario there are many reasons to be optimistic about handle (=wager volume) in the next few years. But that does not mean that there is a lot of revenue up for grabs in the near term, or even that a new entrant in the category could get their hands on much. How can that be? It’s a non-obvious answer, but our perspective is laid out below. And if all this is correct, does it mean that there is nothing to invest in? Hardly. We’ll lay out exactly what we’re hunting for, and we’d love to hear what you think is worth the chase.

You’ve likely heard an estimate of $150bn in illegal betting wager volume thrown around. That number comes from the American Gaming Association[1], estimated in the following way: in 2017, $4.7bn was bet on the Super Bowl, but only $140M of it registered in legal books, ie Nevada. So roughly 97% of betting activity on that event was in the shadows. In that year, Nevada registered a total of $4.9bn in legal sports wager volume, so assuming a similar proportion of illegal to legal activity, $4.9bn was the 3% tip of the iceberg, and another $150bn+ was lurking beneath the surface illegally. There are a couple other ways we can triangulate if you find that estimate a stretch.

For example, UK is a great proxy, and about 17% of their population make a bet in a given year.[2] Coincidentally, Gallup ran a poll in 2008 that estimated that about 17% of Americans place a bet on sports annually[3], which would be about 43M Americans (over 18, of course). About 1M people came through Nevada and made a sports bet legally, so taking that same ratio (1M legal : 43M illegal) we still get a similar 97% shadow market. The upshot is there could definitely be over $150bn in total wager volume across the US to unlock, which at a 5% win rate (rounding down a typical bookmaker’s margin) is about a $7.5bn market.

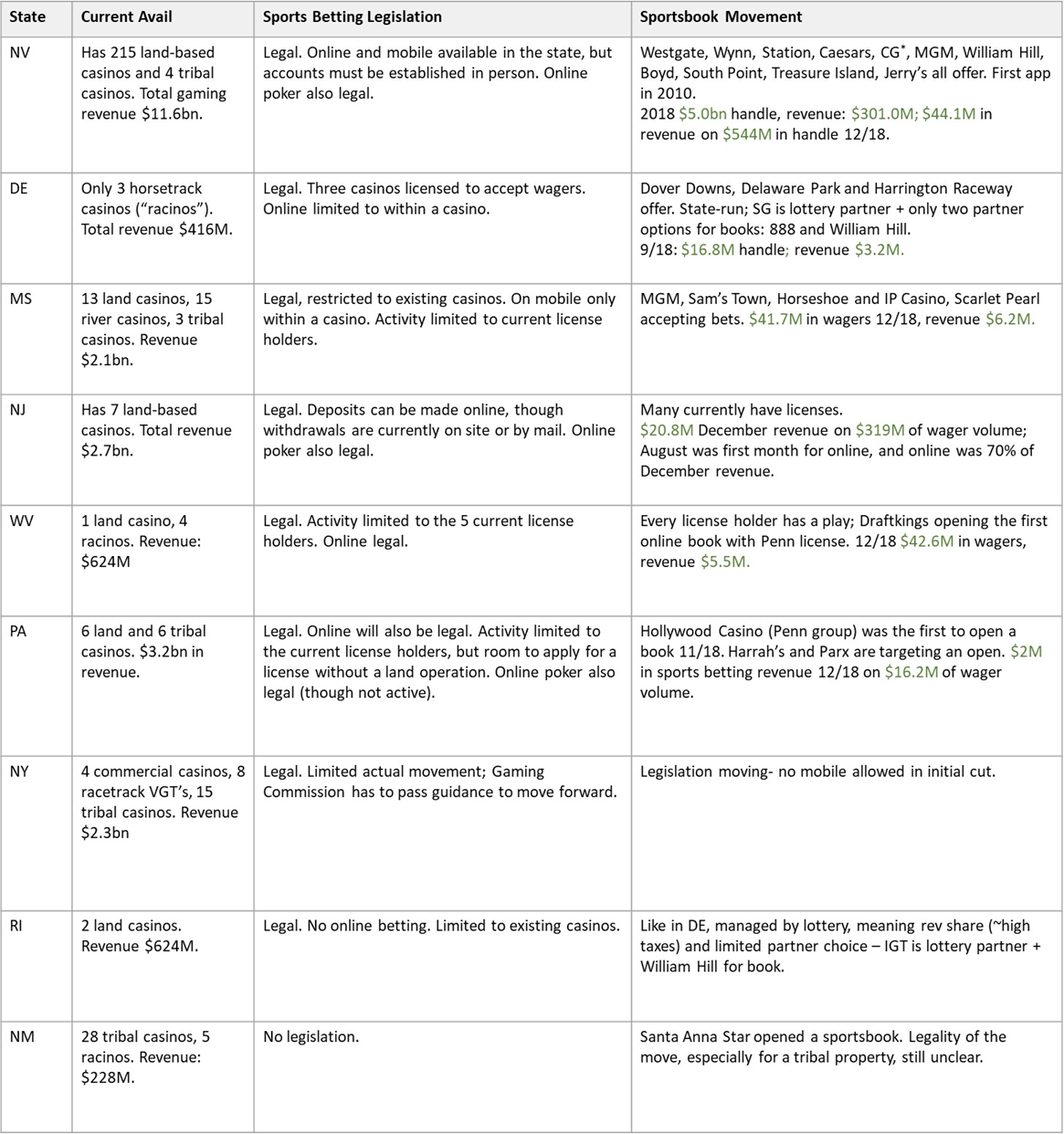

The repeal of PASPA didn’t instantly open up the US to sports betting, it just threw the issue to the states. So, despite the fact that the repeal was last May, today only 9 states- New Jersey, West Virginia, Pennsylvania, Delaware, New York, Rhode Island, Arkansas, Mississippi and Nevada, with some potentially unsanctioned activity in New Mexico — have approved sports betting. There are many contenders for the next rung, including Michigan, Illinois, Connecticut and California, but in each jurisdiction the legislation will face challenges.

One major challenge will slow a lot of states- tribal gaming. Total legal gaming revenue in the US is actually split between state casinos and tribal casinos; only 12 states have no tribal activity. The agreements between the states and the tribes across regions will differ, but generally they have defined what types of gambling can be offered by each group. In some states, like California, exclusivity has been granted to the tribes around specific games. In these cases it isn’t as easy as approving sports betting in the state generally, given the question of who among tribes, land-based casinos, card rooms or riverboats can offer what. In some cases the change will require a reopening of a state constitution.

Outside of time to move through the legislative process, the next largest challenge is what, precisely, is made legal in each state. Only three of the 9 legal states actually offer online wagering outside the geofence of a casino property. This makes sense- casino lobbies in these jurisdictions have limited experience with online/mobile, and have invested materially in their physical locations. Why wouldn’t they lobby to keep consumers betting on the property, and maybe playing the slots while the patrons are there?

But if sports betting isn’t online and mobile, it’s liable to lose as much as half its potential wager volume. Take a look at how sports betting plays out in other countries in the graphic below[4]. In the UK, with $44bn of wager volume, 72% of sports betting is done online. In fact, even looking back on New Jersey’s December 2018 revenue, 70% came from online activity.

Having said all that, it is likely that the current path to legislation, more than lobbying, is skewing the numbers and making it appear as though mobile sports betting won’t find legal footing in the US. Many of the early mover states leveraged older legislation that left the door open for sports betting, so that legislation often lacked support of online initiatives. New legislation in states is likely not to make that mistake, and bills in New Hampshire, Connecticut, Virginia, Indiana, Michigan, Illinois, and Texas have pushed for mobile. In addition, a number of currently active regions, like Rhode Island, are working to bring online/mobile betting to their state.

So now some reality has set in on our $150bn north star. Timing, state legislatures, complications with tribal compacts and especially lack of online access could really dampen our expectations for the next five years. It will change the percent of the US population that has any access and will affect the repatriation rate of all that illegal gambling. Which, even in the rosiest scenarios, is unlikely to be 100%- research suggests that some of the shadow market would like to stay in the shadows, and estimates have a repatriation rate closer 38%.[5] Here’s a much more realistic ramp of what sports book revenues in the US could be.[6]

Before we get off market, one of the questions we focused on here was: “assuming the legal challenges are cleared, how do we expect the US to take to sports betting, culturally?” Many comparisons have looked at the mature UK market and assumed the US would match it, i.e., about a third of all gambling revenues would eventually stem from sports betting, about a fifth of the population would engage with it in some way and it would be heavily mobile. Others argue that in the UK, it was hard to grow up without being assaulted by William Hill ads daily, and that we shouldn’t underestimate many years of illegality for creating a culture of prudence and outright discomfort around gambling here.

Despite all these positive indicators, a cultural feeling of “icky-ness” around gambling makes a dent. Even today, media companies that would otherwise profit by being affiliate partners to bookmakers or from monetizing their own content on bookmaker’s sites hesitate to do so given the public perception, and as a result slow down general adoption.

More important, this culture has made a dent on who would gamble. We took a granular look at perspectives, interviewing a variety of people with all ranges of gambling experience and getting their read- you can see that output in Appendix 1.

What’s interesting here is that in the absence of legal sports betting, a bifurcation has been created between the social culture around watching sports and the culture around gambling on them. Social games like season-long fantasy and Super Bowl Squares surround a love of watching games and are fundamentally more social than interested in winning. Bets make the games interesting more than the other way around, and these folks aren’t eager to gamble against a book even if it becomes legal. On the other side are people who gamble, not just on sports but on many things; these are likely to be daily fantasy players as well. They separate their enthusiasm as fans from what they actually bet on, and generally are out to make money. Compare this all to the UK, where sports fans blend those social and pecuniary ambitions rather better; 46% of people are out to win, with a trailing 34% behind them just in it to have fun.[7]

The thing is, if we can’t build an industry off of the segments currently playing illegally, we are hoping to build this industry on a new generation of US sports bettors, those meant to rise from the sports fans. Their reticence to take a social bet among friends to a bookmaker could slow this market tremendously.

You may be looking at this potential $5bn of betting revenues in 2021 and thinking to yourself “self, that’s a pretty decent sum of money. I should go open a book in West Virginia.” But hold on. What doesn’t get mentioned nearly enough, especially among those who really believe in an enormous burgeoning US sports betting market, is the tough economics of being a bookmaker. Let’s set aside how much infinitely harder it is if you’re an outsider, i.e., not a current gaming license holder or tech partner of such a holder. The truth is, the take rates, or margins, in sports betting are pretty low.

Casinos can make a very healthy profit on their slot machines, and they’re doing very well on Keno (never play that), but Nevada casinos take home about a 6%[8] margin on sports betting, even factoring some better performance on the parlay bets. If you were confused about why casinos would be lobbying against mobile gaming, this is a big part of it- you gambling at home in your pj’s probably doesn’t cover the cost of the team they have in-house setting lines and managing the book.

For a startup, it’s going to be a lot worse. Every open region has their own rules about licensing, but most often the state has already issued a number of gaming licenses, and sports betting will be restricted to the holders of those licenses. Some states, like Nevada and New Jersey, have a path for the issue of entirely new gaming licenses; other states have lax policies on “skins,” or the ability of a new operator to leverage the license of an existing player to build an online presence. Appendix 2 attempts to summarize the current limitations in each open region. Notice that under the same Golden Nugget license in NJ, multiple operators are running a book online. Independent operators or casino gaming groups with limited experience running an online book can choose to build their own (with a partner like SG) or they can offer up their skins for cash / rev shares, or they can do both.

So a startup does have a path, at least in open online markets, but it likely requires a near $10M down payment. That’s assuming you can even find a partner. Slots are going fast and players are rapidly pairing up (think Eldorado’s announcement with William Hill, MGM’s with GVC, etc). But say you do find a friend and land yourself a presence, now you have to compete for customers. In NJ you could be competing with 13 other players, and they are paying (from what we hear) as much as $200 a head to acquire customers.

To recap what we said earlier, you’d be trying to recoup that customer cost from your 6% margins on the wager volume today, which really isn’t much; see chart below.[9] To put it another way, current US gamblers placing sports bets on illegal online sites may spend about $4,285[10] a year, which is about what you’d need to turn a profit with that margin. But remember that these gray market bettors still have relatively little incentive to transfer their bets to legal platforms, and only a few are willing to today. So you’re more likely targeting social bettors, who, if daily fantasy spend is any indication, spend only around $300 a year.[11] The $18 you scrape off of that annually is definitely not going to cut it.

In NJ, basing a run rate on December 2018 revenue figures, you’d be splitting $250M of annual revenue with those 13 competitors. Hardly enough to make back the license cost, much less make a profit on the customers you acquired.

Another challenge is the Wire Act, which basically prevents bets from being taken across state lines. What that practically means is that even if both New York and Illinois were territories in which sports betting was fully legal, and fully legal on mobile, it would be illegal for someone in NY to book a bet for someone in IL. This effectively breaks up an enormous national opportunity into a strictly state-by-state opportunity. It means that not only does a book have to manage the variety of laws and tax codes for sports betting across every state, but they also cannot leverage an established position in one state to make money in another. Not only do they have to set up an operation (and find a partner to give them a skin) in every state, but they also cannot balance their books across states. They cannot offload volume from one state to another, or create an exchange framework like the kind that exists internationally, effectively playing matchmaker and taking a margin to match bettors across both sides of bets.

It does sound dour, but the truth is a well-capitalized player could do well here. Because of the Wire Act and the isolated geographies, each individual territory is hard to make money in, but leveraging states to build national name recognition could definitely pay off, at least over the next five years. FanDuel’s deal with Boyd Gaming, for example, could get them into multiple states Boyd operates in- access to NV, IL, IN, IO, KS, LA, MS… not to mention other states they are cementing with additional partnerships. They are almost certainly losing money as a sportsbook today between the cost of those skins and the heavy cost of customer acquisition, but over time they can build a brand reputation that will make it possible for them to make money across states if not in each of them.

Why? Whether booking sports bets on its own can be profitable or not, sports betting is interesting for another reason. While sports betting may only be 15% of all gambling globally, it represents 50% of online gambling, and 68% of all mobile gambling.[12] Once you have users playing real money on mobile, you can monetize them in many ways- with media (subscription to an OTT sports package?), with advertising, or with other real money online games like poker or slots. Today, the last of those still faces a ton of legal challenges, but you can assume that the largest casino groups are worried about this category because it creates opportunity for newcomers to take share and pull people who now regularly visit physical casinos (and leave some $70bn behind them).

There will definitely be some big winners here, whether it is a newcomer we have not seen, a player like DraftKings, or potentially a consolidated player like Eldorado + Caesars. Can we invest in this? Probably not. This is going to require a hell of a lot of capital.

As we just walked through, any bet on a bookmaker faces a ton of risk, but the biggest risk is likely timing. How long does it take this nascent market to materialize into a few billion of revenue? No idea. But there are bets we can make that have a lot less timing risk.

Today, legal betting in the US is dominated by football and basketball, with baseball pretty far behind. But with the wave of new OTT platforms and cord-cutting, consumers are put in front of a lot more “alternative sports” than just those- surfing, wrestling, esports, etc. Betting on these games will only help drive interest- already League of Legends was DraftKings’ fastest growing sport. Plenty of other dynamics already encourage a dispersion of eyeballs, not least of which is the aging demographics of basketball and football fans, which means advertisers and networks are hunting for alternatives. There is plenty of opportunity in new leagues, new networks, new OTT platforms, etc. that take advantage of that interest.

Already, millennials spend more time out of their homes than previous generations. In addition, cord cutting has meant that many of them are assembling their own entertainment bundles rather than living with an inflated cable bundle with all their sports channels baked in. At the same time, I believe commercial venues are cutting the cord as well, rethinking their costly commercial cable bundles and thinking about streaming alternatives that entertain and engage customers as well as make it possible to throw up alternative options like Twitch.

I think the net effect is more captive out-of-home audiences watching their favorite teams while out, on platforms that are interactive. These would be perfect solutions for in-venue betting. Imagine being in a Buffalo Wild Wings and making a wager on a field goal while you wait for your fries to arrive. Wagering in retail sites is an activity that already drives a good amount of revenue in a different format- video game terminals in restaurants, though a weak proxy, are legal in a few states, and already generate around $1.0bn[13] in revenue for IL alone.

Sports betting is a very different thing than season long fantasy. If you move from left to right in the microsegments (Appendix 1) and reference the second row, you’ll notice how the resources that a bettor leans on vary wildly from what a sports enthusiast follows. In this new territory, ESPN, Bleacher Report, Barstool, etc. have little ground, but the existing media for bettors also leans much more toward the sophisticated gambler (just a page of lines and odds) than the casual one. Some hybrid is bound to emerge, whether its something like the Action Network or someone yet unknown.

Running a book is hardly easy, and there are opportunities to compete with the large platform providers to offer solutions to casino operators to help them stand one up. That said, there are a good number of incumbent players there (SBTech, Kambi, etc), so we are looking for providers with a different edge. One opportunity we didn’t touch much here is around in-game betting, or the prop bets that can be made in-play.

These bets can be a material source of revenue, though internationally they are often concentrated among a small group of avid players. Some estimates suggest as much as 70% of revenue comes from them. Many believe that the US might be a different market; i.e., that the social sports fan may be interested in making the occasional prop bet. More importantly, that fan may not be so particular on the pricing, creating opportunity for significantly higher margin in the space. The challenge is creating those bets, i.e., setting those lines, a task that in many books is handled by mathematicians with complex statistical models assessing risk. This is a costly enterprise, and it would take an army to cover all the activities customers might want to bet- think of the variety of thin markets you’d have to price. A few players are stepping up to solve that challenge, replacing rooms full of traders with algorithms to wisely price fast.

That said, it is likely the majority of books are more focused today on finding partners that can support them in going live, and doing that in as many states as possible as fast as possible. So that likely takes priority to seeking out challenger solutions with exciting new offerings. This is perhaps a category of opportunity that grows over the next few years.

Data is unavoidably valuable in American sports. You can’t watch game coverage without the benefit of live stats and analytics to engage viewers. Assume sports betting does open up across the country and capture many current sports fans as new bettors, you can imagine how much more valuable these data points will be from a media perspective, to differentiate simulcasts and to power all the emerging commentary that will cover betting lines and picks.

But there is much more opportunity that just that on the B2B side. Books setting prices need real-time data to do it. As mentioned in the section above, it’s not just an XML feed of what’s happened that’s necessary, but often a solution that provides opening lines and pricing as well. Today, books rely on packages from the largest providers- players like Sportradar and Genius Sports. In fact, they often have multiple data providers, in addition to their platform providers.

Unfortunately for start-ups, requirements for “official” data help incumbent players maintain their grip on the space. Play data is not necessarily objective data, and a data provider can miss a reviewed call or inaccurately tag a play, compared to a league’s official version of events. Because of this (and an appetite for the large fees involved), leagues have pushed to require official data partnerships and largely cemented those with the large data players.

So what terrain remains? There are a few markets the large guys don’t cover well, like esports. There are are also players developing proprietary data assets that will be uniquely valuable for a given sport, which can plug in nicely into the suite of providers a book is already using, rather than attempting to replace all of a book’s existing systems. There are also players currently serving as sports tech (surfacing player stats for coaching, for example) that can evolve to be unique data asset providers.

Gaming is a highly regulated category. There’s plenty of burden on operators when a patron bets in a venue, but there is a ton of risk to manage online. Not only do betters need to authenticate their age, but they need to be geofenced to the correct state, and their behavior monitored for potential problem behavior. I have run into only GeoComply really tackling this category (though some platform providers include an offering).

It is important to remember that all solutions in the B2B category face the challenge of licensing, as will media companies or free-to-play games monetizing with affiliate revenues. So while we do see a great many interesting start-ups with great D2C platforms or really compelling B2B offerings find early funding, success in this category will ultimately require an ability to meet the regulatory challenges and a fair amount more capital than the average enterprise SaaS effort.

It remains very hard to tell how this nation will embrace sports betting. The next wave of states could struggle and bring forward limited legislation in 2019, or we would see another 10 states adopt mobile sports wagering this year. The average American sports fan could be wary and take years to warm up to the idea or could come around quickly and start booking bets while they sit courtside watching the Lakers. Assuming a mobile-friendly sports betting future in the US, casinos could either use lobbies to dominate this new category, or lose ground to international players or digital-first daily fantasy players with mobile DNA.

It is very hard to guess what is coming, so today we at Jump Capital are more than anything interested in learning. Have a different perspective on the market? Have a company we should take a look at? Is there another segment within this space we haven’t thought of? We’re all ears.

[1] American Gaming Association, 2017 State of the States Report

[2] “A Look Inside the Numbers of Sports Betting in the US and Overseas.” Sports Business Journal, April 2018. Assumes no overlap across online and land.

[3] “One in Six Americans Gamble on Sports.” Gallup, February 2008

[4] Sports Business Journal, April 2018

[5] O’Connor, David. “Sports Betting Will Attract Millenials, Increase Fan Engagement, Hurt Underground Bookies.” Casino.org, 8.15.2018

[6] Eilers & Krejcik Gaming Report 2017. For perspective, Deutche Bank analyst Craig Santarelli had a lower expectation — $4bn by 2023, based on 13 states adopting. H2 Gambling estimates $4.9bn in 2023, with 20 states.

[7] Gambling Participation in 2017 Annual Report, Gambling Commission Feb 2018

[8] Nevada Gaming Control Board Monthly Revenue Report December 2018

[9] Monthly revenues and handle represent December 2018 figures as reported; DE reflects September 2018

[10] Eilers & Krejcik Gaming Report 2017

[11] Fantasy Sports Trade Association

[12] H2 Gambling Capital presentation, G2E event

[13] Illinois Gaming Board

Sources: AGA Report 2018; pending legislation from LegalSportsReport.com

Notes:

Technically OR and MT, like Nevada, have always had the right to offer sports betting, but OR hasn’t offered and MT is rarely mentioned given size. Total revenue refers to last reported annual commercial gaming revenue. Arkansas is omitted; it was the most recent approval and we lack data.

*Cantor Gaming operates the sports books for M, Hard Rock, Tropicana, Cosmo, Venetian, Palazzo, Palms and Silverton.